How lending operations in the Philippines, Kenya, Nigeria, Indonesia, and across high-growth markets in Asia and Africa build automated repayment workflows on channels like SMS, WhatsApp, USSD and more without scaling their collections teams..

Most late loan payments are not a credit problem. They are a communication problem.

Borrowers forget due dates. They lose track of repayment schedules agreed to months earlier. Their salary arrives shortly after a payment deadline and nobody reminded them to prepare in advance. These are not borrowers who cannot pay. They are borrowers who were not reached at the right moment.

For lenders managing thousands of active loans, small improvements in repayment timing have a significant operational impact. Fewer missed payments mean less collections activity, more predictable cash flow, and fewer accounts entering delinquency. As portfolios grow, the difference between a well-performing lending operation and a struggling one often comes down to whether every borrower received the right message at the right time, automatically, without a collections agent doing it manually.

This is why lending operations across the Philippines, Kenya, Nigeria, and Indonesia have shifted from reactive collections communication that begins after a payment is missed to automated reminder workflows that begin before the due date arrives. The intervention happens before the problem exists. That timing difference is where most of the value lives.

What a Loan Payment Reminder System Actually Does

A loan payment reminder system is not just a bulk SMS platform with a scheduler attached. In production lending environments, it is a communication layer connected directly to loan lifecycle events and borrower activity.

The capabilities that matter in practice:

- Scheduled reminders tied to repayment dates

- Automated escalation sequences for overdue accounts

- Two-way messaging that processes borrower responses as workflow inputs

- Payment confirmation handling that stops reminders when a borrower pays

- OTP and identity verification for digital lending workflows

- Delivery reporting at the network level, not just aggregate

- Multi-channel reach across SMS, WhatsApp, and USSD based on borrower availability

The system sits between the loan management system, where repayment data lives, and the collections team, where human judgment is applied to the accounts that actually require it. When these layers are connected properly, collections teams stop spending time on routine reminders and start focusing on restructuring conversations, hardship cases, and high-balance delinquencies.

How Lending Operations Mature Into This

Across markets, lending operations tend to follow a recognizable maturity path.

Stage 1: Manual Reminders. A team member exports a borrower list, uploads it to a messaging tool, and sends reminders manually. No automation, no delivery visibility, no consistency guarantee. This works when portfolios are small. Most lenders hit the ceiling faster than they expect.

Stage 2: Scheduled Communication. Reminders go out automatically at 7 days, 3 days, and on the repayment date. Delivery reports flag failed messages and collections workload drops. Repayment timing typically improves, but overdue accounts still require significant manual handling.

Stage 3: Automated Lifecycle Workflows. Communication becomes event-driven. Disbursement triggers onboarding messages. Upcoming payments trigger reminders. Missed payments trigger escalation. Confirmed payments automatically stop future reminders. Borrower responses like "PAID" or "HELP" initiate different workflows rather than landing in a shared inbox. Collections teams receive only accounts that require human intervention, along with the full communication history that led there. Organizations operating at this level consistently see meaningful reductions in early-stage delinquency because communication consistency no longer depends on manual effort.

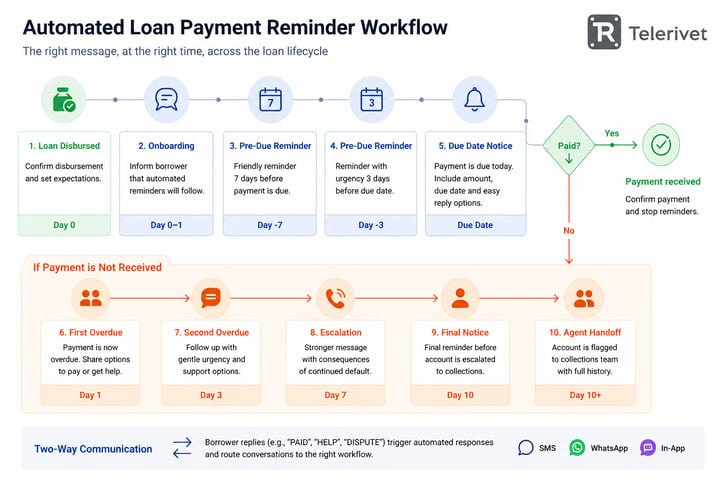

The Borrower Journey That Drives Results

The most effective reminder programs follow a predictable sequence, with timing adjusted for loan type and repayment cycle.

Loan Disbursed ↓ Borrower receives confirmation and repayment schedule

7-Day Reminder ↓ Advance notice to prepare, especially for salary-cycle alignment

3-Day Reminder ↓ Clear repayment amount and due date

Due Date Reminder ↓ Action-oriented message with payment instructions

Payment Received? → Yes: Workflow ends automatically → No: Overdue sequence begins

Overdue Communication ↓ Escalation messages with support options

Collections Team Handoff ↓ Only for accounts requiring direct intervention

For microfinance institutions running weekly repayment schedules, the sequence compresses to two-day and same-day reminders. For salary-linked consumer lending, common across the Philippines, Nigeria, and Indonesia, reminders timed around payroll dates consistently outperform fixed-calendar schedules, based on deployments running this approach across all three markets. Borrowers have available funds when the message arrives.

Why Two-Way Communication Matters

Many lenders focus on sending reminders. The larger operational opportunity is in processing borrower responses.

A borrower replying "PAID" should follow a different path than one replying "HELP." A borrower disputing a balance should follow a different path than one who simply missed the payment. Treating every non-payment event identically creates unnecessary escalations and erodes borrower trust over time.

The most effective systems treat inbound messages as workflow inputs rather than conversations sitting in an inbox waiting for manual review. This is where automated communication starts to function as operational infrastructure rather than a messaging channel.

Market Context: Where the Details Diverge

The workflow logic is consistent across markets. The operational realities are not.

Philippines

The Philippines lending market spans microfinance institutions serving rural borrowers on weekly schedules, salary loan providers running high-volume automated portfolios, and digital lenders where OTP delivery speed is a product requirement rather than a preference. Globe, Smart, and DITO are the primary networks, and delivery performance varies across them therefore network-specific routing visibility matters for operations running at scale.

Regulatory requirements include the Data Privacy Act (RA 10173) administered by the National Privacy Commission, the SIM Registration Act (RA 11934), SEC oversight for lending companies, and BSP oversight for banks and financing companies. Borrower consent for SMS communication should be documented at loan origination. Fair collection guidelines from both the SEC and BSP apply to the content and frequency of collections-stage messages.

Kenya

Kenya's lending ecosystem runs on M-Pesa. Payment confirmation handling is not an optional feature - it is a core operational requirement. The most effective workflows automatically parse mobile money receipts and stop reminders the moment a payment is confirmed. Without this, borrowers frequently receive follow-up messages after paying, which damages trust at scale.

Safaricom dominates coverage, but Airtel Kenya and Telkom Kenya matter for full portfolio reach. For rural and lower-connectivity segments, USSD and SMS remain critical channels. Data protection compliance falls under the Data Protection Act 2019, overseen by the Office of the Data Protection Commissioner.

Nigeria

Nigeria's market operates across four major mobile networks - MTN, Airtel, Glo, and 9mobile with delivery performance that varies significantly between them. Network-level delivery visibility is not a preference in this market; it is an operational requirement for lenders with portfolios distributed across regions. USSD is critical for unbanked and underbanked borrower segments, particularly outside Lagos and Abuja.

Regulatory oversight spans the Central Bank of Nigeria (CBN) for financial services, the Nigerian Communications Commission (NCC) for telecommunications, and the Nigeria Data Protection Regulation (NDPR) for data handling. The CBN has increased scrutiny of collections communication practices in recent years, messaging templates and escalation sequences should be reviewed against current guidance before deployment.

Indonesia

Indonesia combines large rural populations still primarily on SMS with urban segments where WhatsApp penetration is near-universal. High-performing lenders in this market orchestrate both from a single workflow rather than running separate tools. A borrower reachable on WhatsApp gets reminders there first. If delivery fails or there is no response, the workflow falls back to SMS automatically.

Mobile money runs across GoPay, OVO, Dana, and LinkAja, with bank transfer remaining dominant for larger loan amounts. OJK (Otoritas Jasa Keuangan) oversees digital lending and has issued specific guidance on borrower communication practices that peer-to-peer and multifinance lenders must comply with.

What to Look For in a Platform

The features that determine production performance are rarely the ones on the marketing page.

Direct LMS integration via API. Reminder timing should run off live loan data. When borrowers pay, reminders stop. When payments are missed, escalation begins. Manual exports introduce delays that borrowers notice.

Two-way workflow automation. "PAID," "HELP," and silence are three different signals that should generate three different outcomes. Platforms that route inbound messages to an inbox rather than a workflow miss most of the operational value.

Multi-network routing with network-level reporting. Aggregate delivery rates hide the network-specific gaps most likely to affect your portfolio. In Nigeria with four major networks, in the Philippines with three, and across the mixed environments of Asia or Africa, you need to know which networks are delivering and which are not.

Multi-channel orchestration from a single workflow. Managing SMS and WhatsApp from separate systems creates inconsistent borrower experiences and fragmented reporting. The highest-performing operations run both channels from the same workflow logic.

Low-connectivity reach. Routing througha local Android device as well as cloud infrastructure provides resilience for rural borrower segments in environments where connectivity is inconsistent. This matters across all four markets.

Airtime incentives. Early payment rewards tied to airtime disbursement remain underused. In markets where airtime holds real value, automating this as part of a reminder workflow creates measurable lift in repayment behavior.

The Underlying Point

The borrowers most likely to miss a payment are often the ones most likely to pay if reached at the right moment. The collections workload generated by accounts that would have resolved with a well-timed message is real, measurable, and largely preventable.

Organizations that move from manual reminder operations to automated communication workflows find that the primary benefit is not only better repayment performance. It is the ability to redirect collections capacity toward the accounts that genuinely require human judgment, rather than the volume that does not.

A lending operation running automated payment reminders is not doing more communication work. It is automating the work that should never have required people, so the people can focus on what actually does.

Want to see how automated loan payment reminders work in practice? Explore how lenders use Telerivet to build repayment workflows across SMS, WhatsApp, Android Gateway, and other channels from a single communication platform. Telerivet is a multi-channel communication orchestration platform used in more than 150 countries.